Deloitte Canada's oil & gas head says we can expect "another spell of foreign investment."

Mergers and acquisitions in the Canadian energy sector should be robust in 2023 thanks to more stable oil prices, well-performing companies and the pressure to deploy capital, says Andrew Botterilll, national oil, gas and chemicals leader at Deloitte Canada.

“OPEC is making moves to stabilize oil prices around the S80-plus level [Brent and WTI crude per barrel], and we’ve seen strong cash follows, so while energy companies have recently been happy to roll out value to shareholders in the form of dividends, I think we’re going to see some pressure to use those strong balance sheets to support dealmaking,” Botterilll explains.

The result, Botterill says, is that he thinks Canada can expect “another spell of foreign investment.” However, he also wonders whether foreign investment deals are going to necessarily be easy to get done in an environment of increased scrutiny of deals involving foreign state-owned enterprises, U.S. incentives to encourage decarbonization and clean technology for O&G sector south of the border, and what the emerging carbon market will look like here.

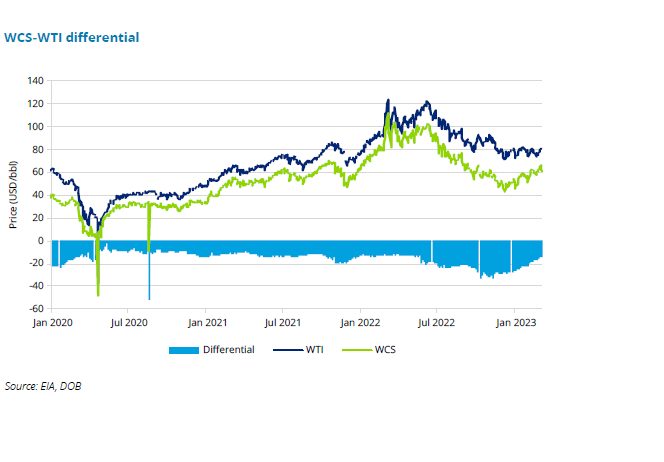

The pricing for Canadian oil is also improving, with a recent Deloitte Canada forecast noting the price differential between WTI and Western Canada Select has significantly narrowed - from more than US$30 per barrel in November 2022 to about US$15 per barrel in March 2023.

Themes for mergers and acquisitions in Canadian oil and gas sector

Deloitte also recently published a report looking at M&A in the energy sector, and Botterill points to some key themes for 2023, which present “a far different picture” than the situation in 2022. For example, last year, M&A in the upstream oil and gas sector struggled as benchmark oil prices surged over US$100, and the gap between buyer and seller valuations widened. M&A spending slumped to 40 percent lower than the previous five years' average.

When deals were not achievable, organizations focused on shareholder dividends, share buybacks, and deleveraging balance sheets. Other factors creating headwinds for deals besides the commodity market were shifting geopolitical priorities and an increased focus on investments in energy transition and decarbonization.

Geopolitical events and economic uncertainty contributed to the volatile energy prices across the globe in 2022. Despite record energy prices and low valuations, M&A activity O&G sector fell to its lowest since 2008. The contradiction is explained in part by the end of the correlation between M&A activity and oil prices as O&G companies remain committed to capital discipline. Instead, free cash flow mpved toward paying dividends and doing buybacks—the old drivers of M&A activity, such as investing and acquiring for growth and increasing market share.

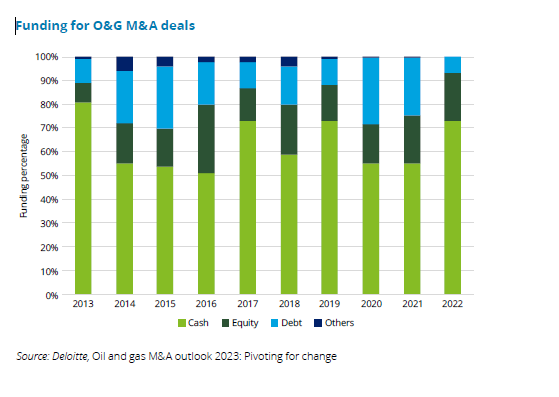

The situation is different now, Botterill says. With reduced debt and record cash flows, operators are now well-positioned to make deals. These healthy balance sheets led to less reliance on external debt for deal financing, with only seven+ percent of sector activity funded through debt in 2022.

“I think we’re going to see companies focused on high-value areas that fit in with the company’s long-term strategies and show synergies and cost efficiencies,” Botterill says, noting that players are still sensitive to recent volatility. “I think companies are going to want resilient, strong portfolios, not just grow for the sake of growing.”

With record free cash flows, the oil and gas sector invested in energy transition. Companies looked to bolster their environment, social, and governance (ESG) scores through partnerships with businesses operating with energy sources such as solar, wind, hydrogen, and biofuel. Despite a dip in 2022, the Deloitte report says strategic investment in the clean energy space is expected to grow over the next ten years as companies seek to meet their ESG targets and perform well on ESG scorecards.

Drivers of M&A going forward

Corporate mergers and joint ventures are expected to continue to outweigh asset acquisitions as companies look to consolidate production and optimize operations. Deloitte’s report on oil and gas M&A, published in February, points to five new drivers of strategic M&A. These include:

Securing energy value chains and trade: Over the past three years, buyers have shown a higher interest in liquid natural gas (LNG) assets to monetize rising exports from the US, higher prices in Europe and Asia, and control the supply chain. Additionally, buyers are acquiring natural gas processing and capacity. Eighty-two percent of global midstream deals were for natural gas-based assets in 2022, in sync with the growing energy security concerns related to fuel. Additionally, the market for integrated purchases and multiple fuels has narrowed and shifted toward specific assets.

Creating partnerships and strategic alliances in shale gas: The U.S. Permian basin accounted for 28 percent of shale M&A activity as players aimed to improve operational efficiencies. However, M&A activity increased in the Marcellus, Eagle Ford, and Bakken basins, (the latter of which includes including Saskatchewan and Manitoba.) Botterill says the Montney Basin in Alberta and B.C. and the Clearwater Basin in Alberta are also shale gas plays that should see deal activity.

The drive for operational excellence in productivity and cost efficiency: Five hundred deals, worth nearly US$171 billion, were made by the O&G industry for clean energy assets between 2010 and 2022, with acquisitions outpacing divestitures by US$43 billion as the industry increased its clean energy presence. The rising focus on an accelerated energy transition helped spur the M&A activity for clean energy assets, with an average deal count of 26 between 2020 and 2022, exceeding the average deal count of 23 recorded between 2010 and 2019. The combination of solar and wind assets remained favoured, accounting for 44 percent of all clean energy M&A since 2010, but more recently, biofuel-related investments are gaining investor interest, with $26 billion worth of deals since 2020.

Governance and compliance with clean energy goals: About one-third of joint ventures and strategic alliances by O&G companies are now in the clean energy space, with the highest number of clean energy joint ventures in hydrogen and related fuels (ammonia, nitrogen, sustainable aviation fuel). Additionally, scope of clean energy joint ventures has broadened to include a mix of sources, fuels, and carbon-capture programs.

Gaining scale and commercializing low-carbon businesses Buyers of O&G assets and companies are increasingly looking for sellers with a higher ESG profile. Over the past five years, in more than 70 percent of deals, the ESG score of the seller was higher than that of the buyer.

Outlook for upstream, downstream, midstream, oil services

Looking at dealmaking in different parts of the energy sector, Botterill says he believes that downstream is “going to continue to be an exciting part of the M&A picture because that’s so much of the investment there will focus on decarbonization – it’s going to be about developing lower carbon fuels, biofuels and sustainable aviation fuel.”

Midstream is another sector that could be ripe for dealmaking, Botterill says, as there isn’t a lot of growth there, “so it’s all about being as efficient as possible and having strong balance sheets.” In the oil and gas service sector, many players have “tightened their belts already and finding themselves relatively busy, but they are struggling to find the skilled workforce they need.

As for upstream dealmaking activity, the Deloitte report notes that M&A activity in 2022 stood at $97 billion, with 207 deals, the lowest since 2005, excluding the pandemic year. Upstream deals declined by 29 percent and 18 percent in terms of value and count between 2021 and 2022, despite average oil prices rising by 43 percent during the same period. This fall in dealmaking likely reflects the shifting priorities toward investing in clean energy M&A.

The oil sands component of upstream production will likely not see a lot of M&A activity for a couple of reasons. Firstly, “we’re down to a very few number players,” he says, “and secondly, there is more investment in projects with a decarbonization component.”

Existing players n the oil sands will likely focus on making their production efficient and cleaner over the long life of bitumen assets.