Firms looking to improve digital platforms, meet ESG goals, invest in areas like wealth management

Deal activity in the financial services sector has been “explosive” since 2020, as institutions explore opportunities to invest capital, make improvements to their digital platforms and operations and adjust activities in the wake of the growing focus on ESG, says a new report by Torys LLP.

Ricco Bhasin, co-head of the firm’s financial services transactions group, says that 2020 was the second busiest year in the sector since the great financial crisis of 2008. But what makes M&A activity in the financial services sector “explosive” this time around, he says, is how the deals “tie into technology, probably more than any other industry area.”

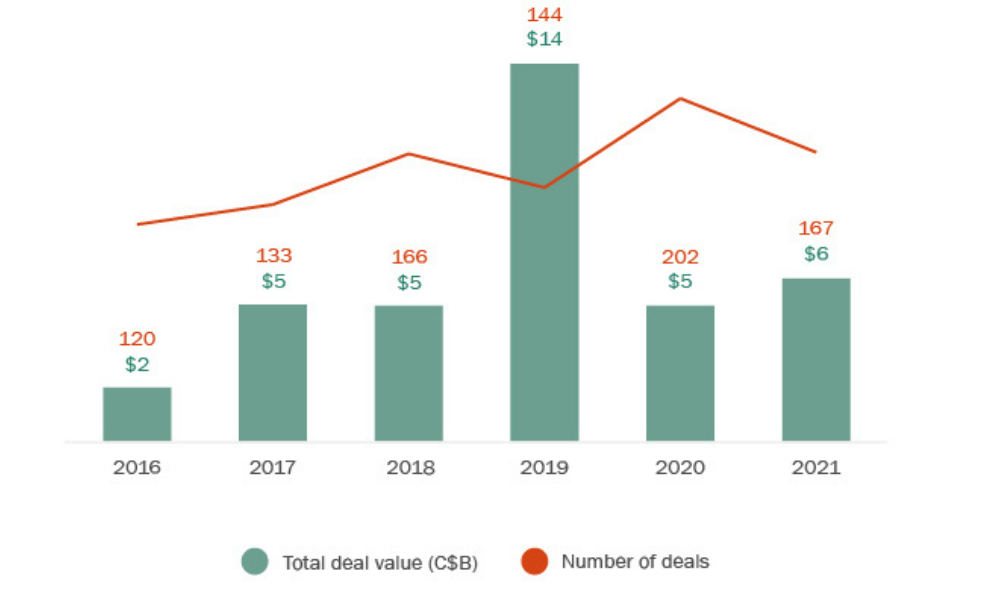

He points to tech-heavy areas such as fintech, robo-investing and data housing, along with more traditional financial services areas such as wealth management. Deal activity has been exceptionally strong in asset management, payments fintech, insurance, banks, loyalty partnerships, and international bancassurance, as set out in the chart below:

Bhasin’s colleague David Seville, co-head of the Torys capital markets practice, notes that financial institutions are generally flush with capital, coming off strong earning and return performances. While some of that money will increasingly go back to shareholders in the form of dividends (which many regulators restricted during the height of the COVID-19 pandemic) or will be used for share buybacks, financial institutions must decide on whether to invest in organic growth or M&A.

Seville also notes that there is “significant private market capital available through pension funds and private equity sponsors to fund growth” by financial institutions.

The Torys report says that M&A will figure large in the growth plans of the financial services industry. A recently released 2022 bank director M&A survey shows that over half of the respondents view M&A as an essential piece of their institutions’ growth in 2022.

However, the report, part of a larger Canadian sector outlook also says that as regulatory regimes continue to evolve to better align with technology and other innovations, “dealmakers in the sector will want to keep watch on changes to regulatory approach, new frameworks and guidance, and changing industry best practices to help mitigate risk.” Specifically, the industry faces increasing accounting, tech, margin, litigation and regulatory pressures.

Bhasin points out that the competition for target companies is fierce. “I think we’ve never seen more buyers in this space,” he says, adding that financial institutions will in some cases be competing with private equity and companies in sectors outside financial services — such as grocery retailers and telecom companies.

“The buyer pool has really become largely a who’s who of the market,” he says, “so when we have auction situations, we’re seeing fierce competition . . . and valuations are soaring.”

In certain jurisdictions, and for certain hot assets, Bhasin says, “we’re seeing up to 15-20 per cent increases [in valuations] when compared to . . . three or four years ago for those financial services targets.”

The report says that while there have been recent examples of blockbuster deals in financial services, notably in mid-market U.S. banking, insurance and asset management, there is increased interest in “roll-up transactions.” These transactions tend to be smaller in dollar value but are playing an important role in the “platform” strategies.

Leading the charge as a material growth area is fintech, along with subsets of this category like insuretech. The report says that “coupled with organic growth and innovation, large financial institutions view these acquisition roll-ups of fintech as critical to having a strong platform, providing superior digital experiences for consumers and…supporting customer acquisition and retention while enjoying economies of scale.”

Still, more traditional financial services transactions remain on the rise as well, including in areas such as banking, wealth management, insurance, lending portfolios and loyalty arrangements. With long-term, steady, and “sticky” returns on capital in financial services, the report says it expects this “high activity trend to continue with market participants not wanting to miss out on opportunities for growth.”

Seville says that “novel transactions” are also shaping capital markets within financial institutions. New structures that are being used to raise capital, including “limited resource capital notes,” offered by Canadian banks (RBC, BMO, and TD among them) and life insurers (Great-West Lifeco) to institutional investors.

The structure in these offerings consisted of two instruments: deeply subordinated interest-paying LRCNs issued to investors; and perpetual, non-cumulative preferred shares issued to a trust to satisfy the recourse of LRCN holders upon the occurrence of certain prescribed recourse events.

The structure of an LRCN offered by Scotiabank in June 2021 added a twist — the instrument issued to the trust is a perpetual note rather than a perpetual preferred share. The ranking of the perpetual notes is higher than that of the perpetual preferred shares, and this is reflected in the non-viability contingent capital (NVCC) multiplier on the perpetual notes of 1.25 versus 1.0 on perpetual preferred shares.

Scotiabank also recently became the first Canadian financial institution to offer US dollar denominated LRCNs with its October 2021 US$600 million offering of 3.635 per cent LRCNs Series 2 notes. The report says the underlying perpetual notes are a “tax-efficient instrument to issue on a cross-border basis.”

Seville says that LRCNs provide banks with a debt instrument but provide “the highest regulatory capital treatment from an OFSI and financial regulatory perspective” This instrument has been “very appealing” to investors, with many returning for subsequent offerings.

Seville also pointed to a new form of preferred share offering targeting institutional investors filed in November by RBC. Unlike the traditional preferred shares historically issued by financial institutions to predominantly retail investors, which are exchange-listed and have a rate reset $25 face amount, the RBC preferred shares have a $1,000 face amount, and are not listed. The distribution is restricted to accredited investors who are not individuals unless they qualify as a “permitted client” under Canadian securities laws.

The substantial face amount, lack of an exchange listing and restricted distribution are consistent with regulatory efforts to encourage institutional rather than retail ownership of so-called “contingent capital” instruments.

This offering was “well received,” Seville says, and “probably sends a signal that maybe other Canadian banks of life insurance companies might offer these preferred shares.”

Both Bhasin and Seville also say the increased focus on environmental, social and governance factors will factor into M&A activity. The Torys report notes that pension funds, banks, insurance companies and other market participants have been announcing ESG commitments, which means buyers of financial services will need to be aware of how this will impact operations and investing. Already, there have been provisions in deal agreements that address ESG issues — how a target company may be operating and what its interests are and how the business model will fold into an organization. Board decision-making may have to balance profits with ESG considerations.

Bhasin also points out that ESG considerations will be important not only in the types of deals are made by financial institutions but also in “how it relates to their client base.” Pension funds such as Caisse de dépôt et placement du Québec and Ontario Teachers’ Pension Plan have announced ESG commitments are two examples.

Says Bhasin: “So financial institutions will have to think hard about acquisitions, and M&A from the perspective of ‘how is it measuring ESG issues, is that method appropriate and will it fit into their ESG structure?’”