Still, concerns about inflation, supply chain and the pandemic could have a stifling effect on deal activity

Coming off a blockbuster year for M&A activity in Canada in 2021, dealmaking in 2022 will likely have a similar trajectory, says John Emanoilidis at Torys LLP. However, a diverse range of drivers could also shape activity in the future.

“I would say it is really among the most active M&A markets in history,” says Emanoilidis, whose firm recently published an outlook on Canadian M&A for 2022. “And it’s not just a Canadian phenomenon, but it’s really a global one.” He adds that based on the pipeline of deals he is aware of, as well as discussions with business leaders, he is “optimistic that 2022 is going to produce another strong year of dealmaking.”

At the same time, Emanoilidis says the protracted disruption caused by the pandemic alongside, as well as decisions and actions made by courts and regulators, are forces that could have knock-on effects on M&A.

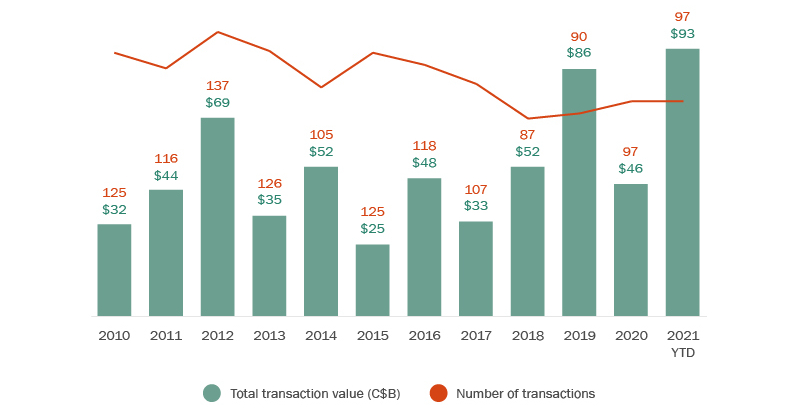

He notes that aggregate deal values for public M&A activity in Canada during 2021 hit a 10-year high of $93 billion. Much of this value was driven by large-value transactions, such as Brookfield Infrastructure Partners’ recently completed acquisition of Inter Pipeline, valued at about $14 billion. Rogers Communication Inc.’s proposed agreement to acquire Shaw Communications Inc. for about $26 billion, and Canadian Pacific Railway Ltd.’s completed purchase of Kansas City Southern for an enterprise value of approximately US$31 billion, are other notable examples of megadeals involving Canadian firms.

In 2021, Canadian outbound M&A activity reached a five-year high in total deal count and aggregate transaction value. The deal activity growth has been notably driven by the increase in the acquisition of U.S. targets, which accounted for 60% of overall outbound deal volume in 2021.

Emanoilidis says the Kansas City Southern was a big deal, but smaller deals also helped acquirers increase their global footprint. For example, Constellation Insurance Holdings, Inc., backed by institutional investors Caisse de dépôt et placement du Québec and Ontario Teachers’ Pension Plan Board, purchased Cincinnati-based Ohio National Mutual Holdings, Inc.

Canadian businesses who are undertaking strategic or transformative transactions underscore the confidence of boards and CEOs in this active deal environment, Emanoilidis says.

“Many companies realized that they did better during the pandemic than they thought they would, so they took a look at the strategic landscape and asking themselves ‘How we can best position ourselves in the current landscape?’”

And while there may be some inflation-related headwinds that could cause interest rates to rise, which could impact dealmaking activity, rates are still relatively low. “So, there’s still lots of liquidity in the system.”

Emanoilidis says that forces in the overall business climate - labour constraints, inflation, supply issues - could have a moderating impact on M&A.

“2022 may not turn out to be as strong as 2021,” he says, “but there are many resilient businesses that will turn out to continue to be attractive targets.” Firms may also try to do deals and lock in financing at attractive rates before “we see a serious increase.”

It’s not just the large deals that were a feature of the Canadian M&A market. Deal activity in the mid-market segment, for transactions valued between $100 million and $500 million grew by 18 per cent, and transactions below $500 million accounted for 75 per cent of all Canadian public M&A deal activity. That’s in line with historical levels where mid-market deal activity has traditionally accounted for the majority of Canadian public M&A transactions.

Canadian Public M&A Market

Source: Bloomberg. Based on transactions involving acquisitions of Canadian public targets announced during Jan 1, 2010 - Dec 7, 2021. Excludes terminated and withdrawn transaction

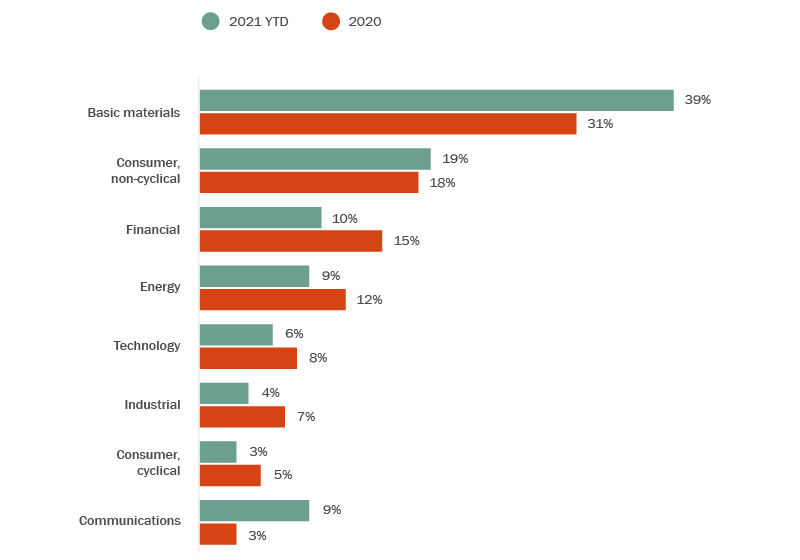

Among the different sectors, Emanoilidis says that the number of deals in the mining industry grew significantly due to high commodity prices. The consumer and financial sectors also attracted a lot of interest. As for the oil and gas industry, despite a decline in activity in 2021, improving commodity prices and a more positive economic outlook point to renewed optimism for this sector.

Spin-offs and divestitures will likely be another feature of dealmaking in 2022, Emanoilidis adds, noting that the Torys’ report says firms will be undertaking more of these deals as a way to “return value to shareholders and refocus their strategic direction.

Public M&A Breakdown by Industry

Source: Bloomberg. Based on transactions involving acquisitions of Canadian public targets announced during Jan 1, 2020 - Dec 7, 2021. Excludes terminated and withdrawn transactions.

He points to H&R REIT recently announcing that it will transform from a diversified REIT into a simplified, growth-orientated REIT. As part of its plan, it will spin out its properties under Primaris, the Canadian retail division of H&R REIT, to create a new stand-alone, publicly-traded REIT focused on owning and managing enclosed shopping centres in Canada.

In another example, George Weston Limited recently announced that it had signed a definitive agreement to sell its Weston Foods fresh and frozen bakery businesses to affiliated entities of FGF Brands Inc. for cash consideration of $1.2 billion.

Many spin-off and divestiture transactions stem from shareholder demands that companies consider optimizing their business portfolios by separating high-growth businesses from low-growth businesses, Emanoilidis says. Or they want to move similar sets of assets into distinct publicly traded entities with the expectation that they will each benefit from more focused management and investor interest as a stand-alone entity.

GE recently announced its plans to spin off its healthcare, renewable energy and power companies to create three public companies, with each potentially benefitting from greater focus and strategic flexibility.

As valuations remain high and market volatility creates potential challenges to price deals, Emanoilidis notes it may become more challenging for some firms to pursue M&A transactions. This may lead to more deals being made with a significant cash component and less stock as currency.

Environmental Social and Governance goals also affect virtually every aspect of M&A transactions, says Emanoilidis, and a driver of deal activity. Businesses are looking to reduce their carbon footprint and find acquisition targets to help achieve net-zero emissions and other related goals.

ESG considerations are seen as essential factors in making deals, not only for the value they can provide but to indicate corporate values and boost reputation. Still, Emanoilidis suggests that acquirers must take due diligence in the screening, valuation, and financing to ensure the deal brings value to the acquirer.